You Invested in becoming debt-free—accelerate your journey with our engaging Debt Repayment Calculator! Experiment with strategies like Snowball or Avalanche, adjust extra payments, and see your payoff timeline update instantly. Explore our timeless financial strategies below to help you stay debt-free and build lasting wealth beyond payoff.

Debt Repayment Calculator

i

How your payments are calculated:

Interest accrues on your full balance at month start

Minimum payments are applied to each debt

Extra payments target your priority debt

Paid-off payments roll over to accelerate remaining debts

Formula:

Monthly Interest = (Balance × APR) ÷ 12

Key Assumptions:

Interest rates remain constant throughout payoff

Minimum payments are 2-3% of balance or $25 minimum

Extra payments applied to principal only

No new debt added during repayment period

Privacy:

All calculations performed locally. No debt data stored or transmitted.

This matches how most lenders process monthly statements

Disclaimer: Results are estimates. Actual payments may vary based on your specific loan terms, payment timing, and lender policies.

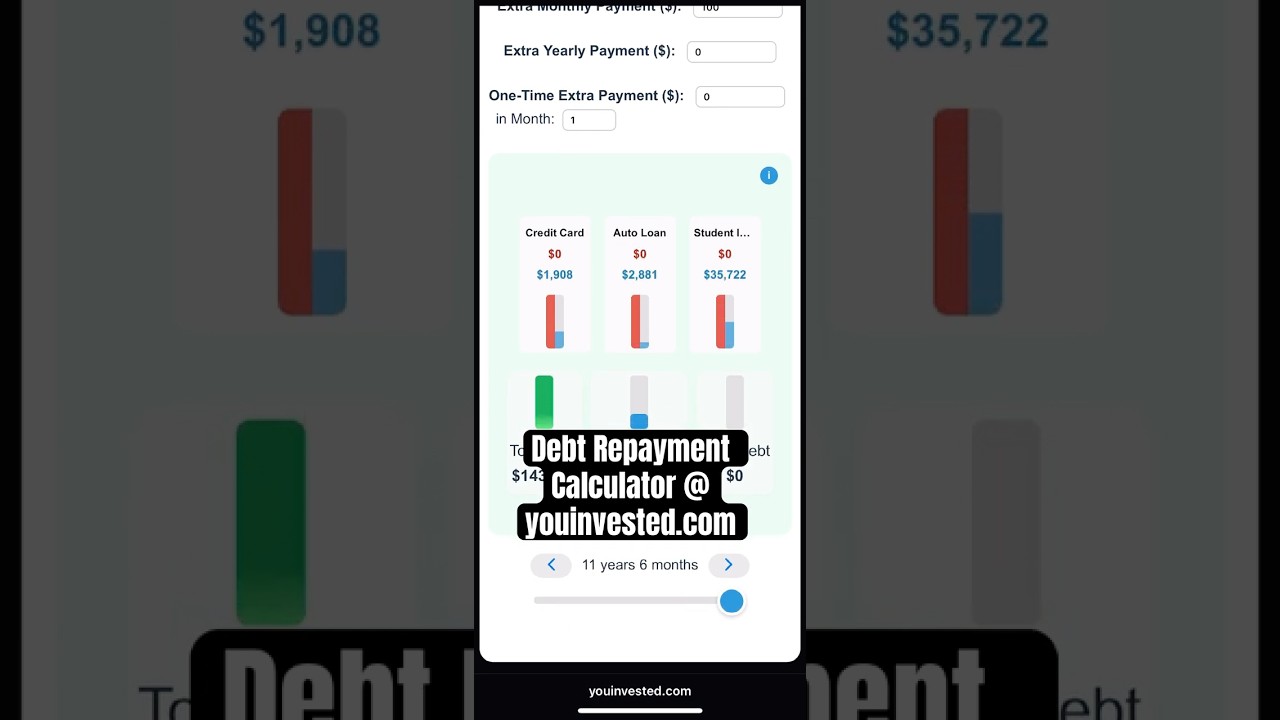

Total Paid

$0

Total Interest

$0

Total Debt

$0

Month 1

See How It Works

Watch our quick demo to see how the interactive debt repayment calculator helps you explore different payoff strategies and make smarter financial decisions.

Chart your course to being debt-free with our interactive calculator. Input your debts and watch your debt-free timeline update in real-time:

Your Debts: List each debt (credit cards, loans) with its current balance, interest rate (APR), and minimum payment. See them combine into a plan!

Payoff Strategy: Choose your method!

Debt Snowball (smallest balance first for quick wins) or

Debt Avalanche (highest interest first to save money). Our tool shows you the impact of each, live.

This isn't just any debt calculator; it's the best interactive planner designed to make debt reduction less daunting and more empowering by showing you real-time results.

Why Use This Calculator

Compare debt snowball and avalanche methods side-by-side with your specific debts. See your exact debt-free date, total interest saved, and payoff timeline update in real-time as you adjust extra payment amounts.

10 Essential Debt Repayment Tips

1. Create a Budget

📊+

Track your income and expenses to understand where your money goes. Allocate specific amounts to debt repayment while ensuring you can cover essential living expenses. Once debt-free, consider redirecting those payments to build your retirement savings with the same discipline.

2. Prioritize High-Interest Debt

📈+

Focus on debts with the highest interest rates first (avalanche method) to save money over time.

3. Use the Snowball Method

🎯+

Pay off smaller debts first for quick wins and motivation, then tackle larger balances.

4. Negotiate with Creditors

🤝+

Contact lenders to request lower interest rates or more manageable payment plans.

5. Consolidate Debt

🔄+

Combine multiple debts into a single loan with a lower interest rate to simplify payments.

6. Cut Unnecessary Expenses

💰+

Reduce spending on non-essentials like dining out or subscriptions to free up cash for debt.

7. Increase Income

📈+

Take on a side hustle, freelance work, or sell unused items to boost funds for repayment.

8. Make Extra Payments

⚡+

Pay more than the minimum whenever possible to reduce principal faster and save on interest.

Set up automatic payments and regularly review your debt reduction to stay motivated.

Understanding Your Live Debt Repayment Plan

Our dynamic tool gives you a clear, live picture of how you can tackle your debts:

Projected Payoff Date: See exactly when you could be debt-free, updating instantly with any change you make. (Visualized by the month slider - up to 100 years).

Total Interest Paid: Understand how much interest you'll pay with different strategies or extra payments – all calculated in real-time.

Strategy Comparison: Compare Snowball vs. Avalanche, updating live by changing the dropdown.

Make a game out of becoming debt-free! This interactive calculator provides the instant feedback you need to stay motivated and achieve your financial goals.

Debt Repayment Planning Guide

Explore common debt repayment scenarios and get the most out of our calculator

Calculate debt snowball vs avalanche payoff comparison

Compare credit card debt consolidation vs current payments

Determine debt payoff timeline with extra payments

Analyze balance transfer impact on total interest paid

Factor in emergency fund building while paying debt

Calculate minimum payment increases to accelerate payoff

Debt snowball vs. avalanche method comparison calculator

Credit card debt payoff calculator with extra payments

How long to become debt-free with my current payments

Personal loan amortization schedule calculator

Visualize debt freedom date with the snowball method

Total interest saved with debt avalanche strategy

Create a debt payoff plan for multiple credit cards

How to pay off $20,000 in credit card debt

Debt consolidation loan vs. current payments calculator

Impact of a one-time lump sum payment on debt

Credit Card Debt Strategy

"Carrying $15,000 across 3 cards? Compare snowball vs avalanche to see which saves more..."

Balance Transfer Decision

"0% APR offer for 18 months? Calculate if balance transfer beats your current payment plan..."

Debt Consolidation Analysis

"Personal loan at 8% vs credit cards at 22%? See your total savings with consolidation..."

Emergency Fund vs Debt Payoff

"Should you build $1,000 emergency fund first or pay minimums and attack debt? Calculate both scenarios..."

Extra Payment Strategy

"Tax refund of $3,000? See how lump sum vs monthly extra payments affects your timeline..."

Before choosing between debt snowball and avalanche methods

When considering debt consolidation options

Before accepting balance transfer offers

When planning extra payments from windfalls

Comparing personal loan vs credit card payments

Planning debt payoff with emergency fund building

Frequently Asked Questions

Get instant answers about debt repayment strategies and how our calculator can help you become debt-free faster.

Our calculator provides real-time, interactive comparisons between the Snowball and Avalanche debt repayment methods. You can see exactly how each strategy affects your payoff timeline and total interest paid, with visualizations that update as you adjust your debts and payments.

It depends on your personality. The Debt Avalanche method (paying off highest interest rates first) will save you the most money in interest and is mathematically the fastest. The Debt Snowball method (paying off smallest balances first) provides quick psychological wins that can keep you motivated. Our calculator lets you instantly compare both to see which is right for you.

AI can give you general advice, but our interactive tool lets you input your specific debts and explore different payoff strategies with live, visual feedback. You can see your debt-free date change instantly as you adjust extra payments—an experience AI cannot replicate.

By using the "Extra Monthly Payment" input, you can instantly see how much faster you can become debt-free. The calculator automatically applies this extra amount to your target debt (based on your chosen strategy) and recalculates your payoff date and total interest saved in real-time.

Absolutely. This calculator is designed for multiple debts. You can add credit cards, auto loans, personal loans, and more. The tool will then create a single, optimized payoff plan based on your chosen strategy (Avalanche or Snowball).

The calculations are highly accurate based on the numbers you provide. They use standard financial formulas to model interest and payments. You can trust them for planning and motivation. However, for severe debt problems, always consider consulting a non-profit credit counselor for personalized advice.

Yes. By setting the "Extra Monthly Payment" to $0, the calculator shows you the long and expensive road of only paying the minimums. This is a powerful way to see how much time and money a focused payoff strategy can save you.

Yes. First, calculate your current payoff plan with all your individual debts. Then, remove all debts and add a single new debt representing the consolidation loan (total balance, new interest rate, and new minimum payment). You can then compare the total interest you'd pay with consolidation versus your current debts. Consider consolidating multiple high-interest debts into a single, lower-interest loan. This can simplify payments and reduce interest costs. Homeowners might explore home equity options or auto owners could consider refinancing to secure better rates. Always compare the total interest you'd pay with consolidation versus your current debts.

The fastest and cheapest way to pay off credit card debt is the Debt Avalanche method. Since credit cards typically have the highest interest rates, this strategy targets them first, saving you the most money on interest and getting you out of debt sooner. Select "Avalanche" in the calculator to see this in action.

The debt snowball method focuses on building momentum. You list your debts from the smallest balance to the largest. You make minimum payments on all debts, but put any extra money towards the smallest one. Once it's paid off, you "roll" the payment you were making on it into the next-smallest debt. This creates a snowball effect as your payments grow larger over time.

The debt avalanche method focuses on saving money. You list your debts from the highest interest rate to the lowest. You make minimum payments on all debts, but put any extra money towards the one with the highest interest rate. Once that's paid off, you attack the debt with the next-highest rate. This method is mathematically guaranteed to save you the most money in interest.

Your debt-to-income (DTI) ratio is your total monthly debt payments divided by your gross monthly income. Lenders generally prefer a DTI of 36% or less. A DTI above 43% can make it difficult to qualify for new loans, so paying down debt is a great way to improve your financial health.

A debt consolidation loan can be a good idea if you can get a new loan with an interest rate that is lower than the average rate of your current debts. This can simplify your payments and save you money. However, it doesn't solve the spending habits that led to the debt. Use our calculator to see if the math works in your favor.

It can be challenging, but it's possible. The key is to create a strict budget to free up as much cash as possible. Even an extra $20 or $50 a month can make a difference. The snowball method is often recommended in this situation, as the quick wins can provide crucial motivation. Also, look for any opportunities to temporarily increase your income.

Good debt is typically an investment that can increase your net worth over time, like a mortgage or a student loan. Bad debt is used for consumption or for assets that depreciate in value, and it often comes with high interest rates. Credit card debt is the most common example of bad debt.

💳 Perfect Complement to AI Advice: Use AI to understand debt strategies and get general payoff guidance, then use our interactive tool to apply those strategies to your specific debts. Slide through payment amounts, compare avalanche vs snowball methods, and visualize how each approach affects your elimination timeline - creating a complete debt freedom plan that combines AI's knowledge with personalized scenario testing. See how compound interest works against you with debt and how you can make it work for you with smart investing.