You Invested in your retirement—now visualize your financial freedom with our comprehensive Retirement Calculator! Plan the way you'll actually live in retirement by Monthly Income, not just a lump sum total.

Adjust your age, income, savings rate, and expected returns to see your personalized retirement roadmap. Our calculator shows your projected monthly income including Social Security, so you can see if you're on track to maintain your lifestyle. Plus, explore our complete guide below—learn strategies for catch-up contributions, tax-advantaged accounts, and making your nest egg last.

Key Assumptions:

• 75% income replacement (adjustable)

• Social Security: 40% of current income

• 7% annual returns pre-retirement, 4% post-retirement

• 3% inflation rate

• 4% withdrawal rule in retirement

Privacy: All calculations performed in your browser. No financial data stored.

This calculator uses compound interest calculations with inflation adjustments to project your retirement savings and determine if you're on track for your retirement goals.

Calculating your retirement readiness...

Future Monthly Income Needed

i

75% of your current monthly income, adjusted for inflation at retirement. This is the standard recommendation for maintaining your lifestyle.

$0

Projected Monthly Income

i

Your estimated monthly income from retirement savings (using 4% withdrawal rule) plus Social Security benefits (estimated at 40% of current income).

$0

From savings + Social Security

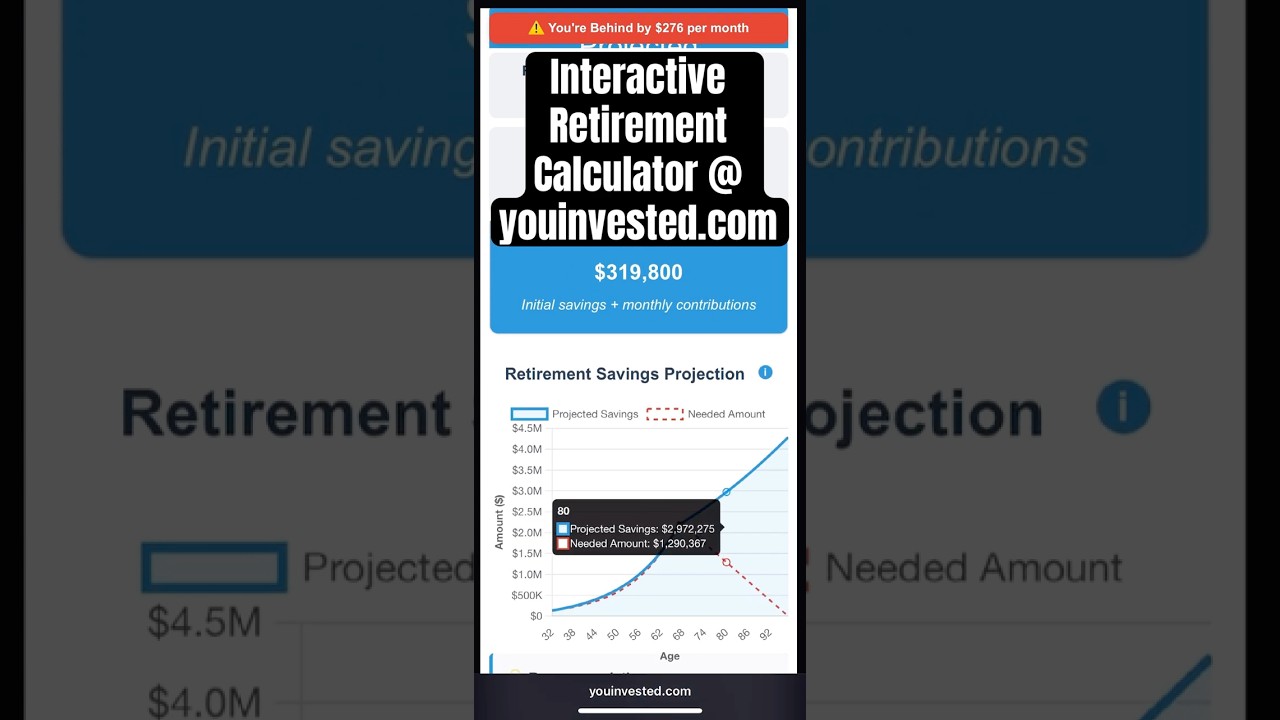

Projected Retirement Savings $0.00

Total Contributions

$0.00

Initial savings + monthly contributions

Retirement Savings Projection

i

Projected Savings shows your estimated retirement savings over time based on your current contributions and expected returns.

Needed Amount represents the target you need to reach to maintain your desired retirement lifestyle, accounting for inflation and withdrawals.

💡 Recommendation

See How It Works

Watch our quick demo to see how the interactive retirement calculator helps you explore different retirement scenarios and make smarter financial planning decisions.

Our interactive retirement calculator goes beyond basic projections to give you a complete picture of your retirement readiness. Here's what makes it powerful:

Real-Time Status Updates: Get instant feedback on whether you're on track, ahead, or behind your retirement goals. Our status indicator changes color to give you immediate visual confirmation of your progress.

Comprehensive Income Planning: See both sides of the equation - how much monthly income you'll need in retirement (adjusted for 3% annual inflation) and how much you're projected to have from your savings plus Social Security benefits.

Flexible Scenarios: Experiment with different retirement ages, income replacement ratios, contribution amounts, and investment return expectations. Every adjustment instantly updates your projections.

Visual Progress Tracking: Our interactive chart shows your savings growth over time, including what happens during retirement years with the 4% withdrawal rule applied.

Smart Recommendations:When you're behind on your goals, the calculator automatically suggests how much to increase your monthly contributions to get back on track.

Projected Retirement Savings: Your retirement goal. Adjust to see how long it will take to reach your desired amount.

Key Calculator Features

Personalized Assumptions

Income Replacement: Default 75% of current income (adjustable 30-150%)

Social Security: Estimated at 40% of current income

Withdrawal Strategy: Uses the proven 4% rule for retirement income

Why Use This Calculator

See if you're on track for retirement with projections that include Social Security estimates and show your future monthly income, not just a lump sum. Test different contribution amounts, retirement ages, and return rates to find your personalized path.

Top 10 Retirement Savings Tips

1. Start Early

⏰+

Begin saving as soon as possible to maximize compound interest calculator over time. The earlier you start, the more time your money has to grow. Use our compound interest calculator to see how it can work for you with different starting ages and contribution levels.

Example: Our calculator shows this dramatically: a 25-year-old saving $500/month reaches $1.2M by 65 with 6-7% return rate, while waiting until 35 reduces this to just $540K—despite contributing only $60K less total.

2. Maximize Employer Plans

💼+

Contribute to a 401(k) or similar plan, especially to capture any employer match. This is essentially free money for your retirement.

Tip: If your employer offers a 50% match up to 6% of salary, contributing 6% effectively gives you a 50% return on that money.

3. Use IRAs

💰+

Open a traditional or Roth IRA to diversify savings with tax advantages. Choose based on your current and expected future tax brackets.

Traditional IRA: Tax-deductible now, taxed in retirement. Roth IRA: No tax deduction now, tax-free withdrawals in retirement.

4. Automate Contributions

⚙️+

Set up automatic transfers to retirement accounts to ensure consistent saving. This helps avoid the temptation to spend elsewhere.

Tip: Schedule contributions for the day after your paycheck arrives to ensure they happen before other expenses.

5. Increase Contributions Over Time

📈+

Gradually raise your savings rate, especially with pay raises or bonuses. Even small increases can make a big difference over time.

Example: Increasing your contribution rate by 1% annually can boost your retirement savings by 25% over 30 years.

6. Diversify Investments

🔄+

Spread your investments across different asset classes to manage risk. A well-diversified portfolio can help protect against market volatility. Use our stock investment calculator to explore different investment strategies to find the right balance for your retirement goals.

Tip: A balanced portfolio of 60% stocks and 40% bonds can provide growth while reducing volatility.

7. Minimize Fees

💸+

Choose low-cost investment options like index funds to keep more of your returns. Fees can significantly impact long-term growth.

Example: A 1% fee on a $500K portfolio costs $5,000/year. Over 30 years, this could reduce your final balance by $200K+.

8. Avoid Early Withdrawals

🚫+

Resist tapping retirement accounts to preserve long-term growth and avoid penalties. Keep your retirement funds for retirement. If you're facing financial hardship, consider using our debt repayment calculator to explore better alternatives to early withdrawals.

Warning: Early withdrawals before age 59.5 can trigger a 10% penalty plus taxes on the withdrawn amount.

9. Plan for Healthcare Costs

🏥+

Save in a Health Savings Account (HSA) or budget for future medical expenses. Healthcare costs can be a significant retirement expense.

Tip: HSAs offer triple tax benefits - tax-free contributions, growth, and withdrawals for qualified medical expenses.

10. Review and Adjust Regularly

🔄+

Check your retirement plan annually to align with goals, inflation, and life changes. Stay proactive about your financial future.

Tip: Rebalance your portfolio annually to maintain your desired asset allocation and risk level.

Complete Retirement Planning Guide

Your comprehensive resource for retirement planning strategies and insights

The 75% Rule - And When to Break It

Our calculator defaults to 75% of your current income because most retirees experience reduced expenses:

No more retirement contributions (you're withdrawing instead)

The calculator estimates Social Security at 40% of current income, which is realistic for middle-income earners. Key facts:

Full retirement age varies: 66-67 depending on birth year

Early claiming reduces benefits: Starting at 62 gives you ~75% of full benefit

Delayed claiming increases benefits: Up to 132% if you wait until age 70

Benefits are inflation-adjusted: They increase with cost of living

Accumulation Phase (Pre-Retirement)

Default assumption: 7% annual returns

This reflects a growth-oriented portfolio suitable for long-term investing:

Stock-heavy allocation: 70-90% stocks in your 20s-40s

Gradual shifting: Move toward 60-70% stocks in your 50s

Diversification matters: Mix of domestic, international, and emerging markets

Low costs essential: Index funds typically outperform actively managed funds

Sample Portfolio for Ages 25-45:

80% Stock Index Funds

15% Bond Index Funds

5% International/Emerging Markets

Distribution Phase (Retirement)

Default assumption: 4% annual returns

This reflects a conservative, income-focused portfolio:

Capital preservation: Priority shifts from growth to protecting principal

Regular income: Focus on dividends, interest, and planned withdrawals

Sample Portfolio for Ages 65+:

50% Diversified Stock Funds

40% Bond Index/Treasury Bills

10% Cash/Money Market

How It Works

The 4% rule suggests withdrawing 4% of your retirement portfolio's value in the first year, then adjusting that dollar amount for inflation each subsequent year.

Exceptional returns: You might increase withdrawals or leave more for heirs

Health changes: Major medical needs might require higher withdrawals

Longevity: If you're likely to live past 95, consider 3.5% rule

401(k) and 403(b) Plans

Contribution Limits:

Under 50: Typically in the low to mid-$20,000s (e.g., $24,500 in 2026)

50 and older: Standard catch-up of $8,000 (or $11,250 for ages 60–63 if plan allows)

Important: All limits are adjusted annually for inflation. Always verify current figures at irs.gov or consult a tax advisor.

Strategies:

Always capture full employer match

Consider Roth 401(k) if available and you're in lower tax bracket

Don't cash out when changing jobs—roll over to IRA

Individual Retirement Accounts (IRAs)

Contribution Limits:

Under 50: Typically in the low to mid-$7,000s (e.g., $7,500 in 2026)

50 and older: Additional catch-up of $1,000+ (e.g., $1,100 in 2026)

Note: Roth IRAs have income eligibility limits. Consider backdoor Roth conversions if ineligible due to high income.

Important: All limits are adjusted annually for inflation. Always verify current figures at irs.gov or consult a tax advisor.

Traditional vs. Roth Decision:

Traditional IRA

Tax deduction now, taxed in retirement

Good if: You're in higher tax bracket now than expected in retirement

Roth IRA

No deduction now, tax-free in retirement

Good if: You're young or expect higher tax rates in retirement

Health Savings Accounts (HSAs)

Triple tax advantage:

Tax-deductible contributions

Tax-free growth

Tax-free withdrawals for qualified medical expenses

Current Limits:

Individual: Typically in the low to mid-$4,000s (e.g., $4,400 in 2026)

Family: Typically in the mid-$8,000s (e.g., $8,750 in 2026)

55+ catch-up: Additional $1,000

Note: HSAs require enrollment in a high-deductible health plan. Consider using HSAs as retirement tools by investing contributions and paying medical expenses out-of-pocket when possible.

Important: All limits are adjusted annually for inflation. Always verify current figures at irs.gov or consult a tax advisor.

In Your 20s and 30s

Primary Goals: Build the foundation

Start with employer 401(k) match

Open Roth IRA for additional savings

Aim for 10-15% total savings rate

Focus on growth investments

Use our calculator to see compound interest power

Calculator Exercise: Compare starting at 25 vs. 35 with same monthly amount

In Your 40s and 50s

Primary Goals: Accelerate and optimize

Increase savings rate to 15-20%

Maximize 401(k) contributions

Use catch-up contributions after 50

Begin shifting to more conservative investments

Consider tax diversification (mix of traditional and Roth)

Calculator Exercise: Model working 2-3 extra years and see the impact

In Your 60s

Primary Goals: Fine-tune and prepare

Maximize catch-up contributions

Plan Social Security claiming strategy

Shift to capital preservation mode

Create withdrawal strategy

Consider healthcare and long-term care insurance

Calculator Exercise: Test different retirement ages and Social Security claiming strategies

1. Underestimating Healthcare Costs

Healthcare expenses often increase in retirement. Consider:

Medicare premiums and gaps

Long-term care potential

Prescription drug costs

Dental and vision care

2. Ignoring Inflation

A 3% inflation rate doubles costs every 23 years. Our calculator automatically adjusts for this, but many people forget inflation's impact on fixed incomes.

3. Too Conservative Too Early

Being overly conservative in your 20s-40s can cost hundreds of thousands in growth. Use our calculator to see how different return assumptions affect your final result.

4. Not Planning for Taxes

Consider your tax situation:

Traditional retirement accounts are taxed in retirement

Roth accounts provide tax-free income

Social Security may be taxable depending on other income

Plan for required minimum distributions starting at 73

5. Lifestyle Inflation Without Savings Inflation

As your income grows, increase your savings rate proportionally. Use our calculator's contribution slider to see how small increases compound over time.

Frequently Asked Questions

Get instant answers about retirement planning and how our calculator can help you make wise financial decisions.

Unlike traditional retirement calculators that require you to hit "calculate" after each change, our interactive tool shows real-time results as you adjust any input. Watch how increasing your monthly contributions by just $100 or working a few extra years can dramatically impact your retirement piggy bank. The instant visual feedback helps you understand the power of compound interest and make better long-term decisions.

Yes! Our interactive calculator includes live contribution sliders that instantly show how increasing your monthly or annual contributions can grow your retirement savings. As you adjust the contribution amount, you'll see the immediate impact on your projected balance, helping you find the right savings rate for your goals.

Our calculator estimates Social Security benefits at 40% of your current income, which aligns with average replacement rates for middle-income earners. For more precise estimates, check your Social Security statement at ssa.gov, but our calculation provides a solid baseline for retirement planning.

AI provides general retirement advice and calculations, but our interactive tool lets you explore contribution scenarios with sliders, see compound growth visualizations, and model different retirement ages in real-time - all unavailable through AI text responses. The immediate visual feedback helps you understand the impact of each financial decision on your retirement goals.

Adjusting the retirement age slider shows you the powerful impact of working longer. Each additional year means more time for your investments to grow and fewer years of withdrawals to fund. Our calculator helps you visualize how just a few more years of work can significantly boost your retirement security.

Our calculator lets you adjust expected returns to see how market performance affects your retirement. Try different scenarios to understand how conservative or aggressive investment strategies might impact your piggy bank. This helps you make informed decisions about your portfolio's risk level.

Include employer matches in your contribution amount to see their significant impact. For example, if you contribute $500 monthly with a 50% employer match, input $750 as your total monthly contribution. The calculator will show how this "free money" accelerates your retirement savings over time.

All future dollar amounts in the calculator are automatically adjusted for 3% annual inflation, so your "future income needed" represents the buying power equivalent of today's dollars. This ensures your projections remain realistic in terms of actual purchasing power.

Most financial experts recommend 70-80% of pre-retirement income because certain expenses typically decrease in retirement (commuting, work clothing, retirement savings contributions). However, you can adjust this percentage based on your specific retirement lifestyle plans.

The 4% rule is a guideline suggesting you can safely withdraw 4% of your retirement savings in the first year of retirement, and then adjust that amount for inflation in subsequent years. This strategy aims to make your money last for 30 years or more. Our calculator helps you see if your projected savings align with this rule.

Financial experts often suggest benchmarks for retirement savings. For example, Fidelity recommends having 3x your salary saved by age 40, 6x by age 50, and 8x by age 60. These are general guidelines, and our calculator can help you create a personalized plan to reach your specific goals.

The 7% default reflects long-term historical stock market averages, but you can easily adjust both pre-retirement and post-retirement return expectations using our sliders. Conservative investors might use 5-6%, while more aggressive investors might project 8-9%.

A "good" rate of return depends on your risk tolerance and investment strategy. Historically, diversified stock portfolios have averaged around 7-10% annually over the long term, while bonds and cash offer lower but more stable returns. Our calculator allows you to experiment with different return rates to see their impact on your projected savings.

Retiring early typically requires aggressive saving, higher investment returns, and potentially a lower spending rate in retirement. Our calculator can help you model different scenarios by adjusting your current age, retirement age, contributions, and expected returns to see what it would take to achieve early retirement.

A Roth IRA is a retirement savings account where you contribute after-tax dollars. Your contributions and earnings then grow tax-free, and qualified withdrawals in retirement are also tax-free. This is ideal if you expect to be in a higher tax bracket in retirement than you are now.

A 401(k) is an employer-sponsored retirement plan that allows employees to save and invest a portion of their paycheck before taxes are taken out. Many employers offer a matching contribution, which is essentially free money for your retirement. Your money grows tax-deferred until you withdraw it in retirement.

🏖️ Perfect Complement to AI Advice: Use AI to understand retirement concepts and get general savings guidance, then use our interactive tool to model those concepts with your specific numbers. Slide through contribution amounts, visualize how compound growth accelerates your nest egg, and explore different retirement age scenarios - creating a complete retirement plan that combines AI's expertise with personalized financial modeling. See how compound interest can accelerate your retirement savings, or explore investment growth scenarios to optimize your retirement portfolio.