You Invested in your dream home—explore the costs with our dynamic Mortgage Calculator! Tweak home price, down payment, interest rate, loan term, or HOA fees, and see your monthly Principal, Interest, Taxes, and Insurance costs update instantly. When your down payment is less than 20%, our calculator automatically shows PMI (Private Mortgage Insurance) costs too. Explore our timeless homebuying content below for insights on down payments, refinancing strategies, and building long-term wealth.

Interactive Mortgage Calculator

Monthly Payment

$0.00

Total Interest Paid

$0.00

Total Amount

Principal + Interest

$0.00

$

%

ℹ️PMI (Private Mortgage Insurance) is being applied to your mortgage payment (approximately $0/month). Adjust PMI rate or disable the toggle in Advanced Options to exclude PMI.

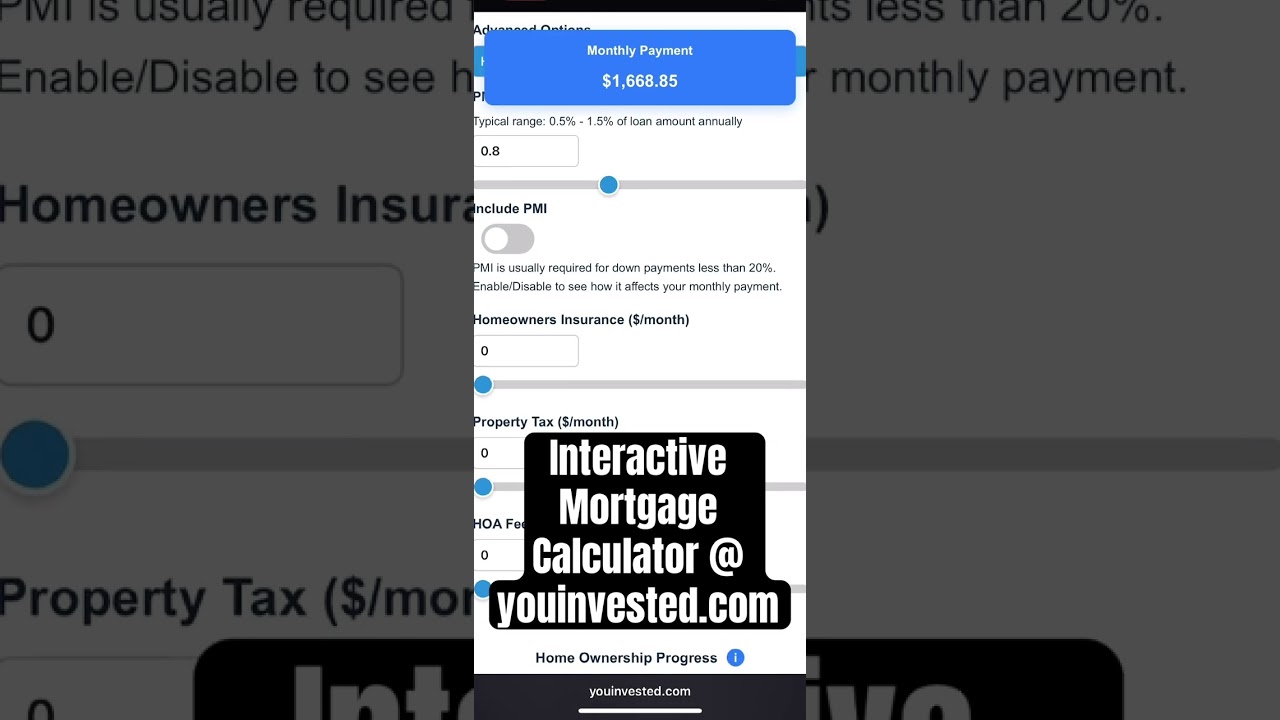

Typical range: 0.5% - 1.5% of loan amount annually

PMI is usually required for down payments less than 20%. Enable/Disable to see how it affects your monthly payment.

Home Ownership Progress

i

How Your Mortgage is Calculated:

Enter the home price, down payment, interest rate, and loan term

Monthly payments are calculated using the standard mortgage payment formula

Extra payments are applied directly to the principal

Interest is calculated monthly on the remaining balance

Formula:

P × [r(1+r)^n] / [(1+r)^n - 1]

Where P = loan amount, r = monthly rate, n = total months

Key Assumptions:

PMI automatically applied when down payment < 20%

PMI removed at 80% loan-to-value ratio

Fixed interest rate for entire loan term

Extra payments applied directly to principal

Privacy:

Calculations performed in your browser. No data transmitted.

Disclaimer:

This calculator provides estimates only. Actual loan terms may vary based on creditworthiness, property location, and lender requirements. Please consult with a mortgage professional for personalized guidance.

Principal: $0.00

Interest: $0.00

Remaining Balance: $0.00

Year 1

See How It Works

Watch our quick demo to see how the interactive mortgage calculator helps you explore different loan scenarios and make smarter home financing decisions.

Getting your live mortgage payments is easy with our dynamic calculator. Simply input your figures, and watch the numbers adjust in real-time:

Home Price: The purchase price of your future home. This helps determine the loan amount.

Down Payment: Your upfront amount. Play with different percentages or dollar amounts to see immediate changes to your monthly payments.

Loan Term (Years): Typically 15 or 30 years. Witness the difference in monthly payments and total interest as you adjust.

Interest Rate (%): Your expected annual interest rate. Even a 0.5% difference can save thousands - for example, on a $300,000 loan, the difference between 6% and 5.5% is $87/month, or $31,320 over 30 years—see it live!

Monthly Extra Payment ($): Add extra payments to your mortgage to pay it off faster. Adjust this slider to see how it impacts your total payments and payoff time.

Advanced Options: Expand to see additional inputs for homeowners insurance, property tax, HOA fees, and PMI controls. Adjust these to see how they affect your monthly payments, and use the PMI toggle to compare scenarios with and without PMI.

Understanding Your Live Mortgage Breakdown

Your core mortgage payment consists of two main parts. Our interactive calculator shows you these components live:

Principal (P): The portion of your payment that goes towards paying down the actual loan amount borrowed.

Interest (I): The cost of borrowing the money, paid to the lender. See how it changes with different rates and terms in real-time.

Make home loan planning less of a chore and more of an exploration. This interactive mortgage calculator is designed to empower you with instant insights into your primary loan costs!

Why Use This Calculator

To test multiple scenarios instantly - see how different down payments affect PMI costs, compare 15-year vs 30-year loan impacts, and visualize how extra payments reduce total interest. Interactive exploration beats one-time calculations for major financial decisions.

Buying a home is one of the biggest investments you'll ever make. This guide will demystify the core concepts of your mortgage, so you can use our calculator with confidence and make the smartest financial decisions for your future.

The Four Pillars of Your Mortgage Payment: PITI

Your monthly mortgage payment is more than just the loan repayment. It's typically composed of four parts, known as PITI:

Principal (P): This is the amount you borrowed from the lender. Every month, a portion of your payment goes toward reducing this balance.

Interest (I): This is the cost of borrowing the money, paid to the lender. In the early years of your loan, a larger portion of your payment goes to interest.

Taxes (T): These are property taxes, which your lender usually collects from you monthly and holds in an escrow account to pay on your behalf.

Insurance (I): This refers to homeowner's insurance, which protects your home against damage. Like taxes, these premiums are typically paid from your escrow account.

Try It Now: See how these numbers come together! Click the "+Show Advanced Options" button in our calculator above to input your estimated property tax and homeowner's insurance. Watch your total monthly payment update instantly.

Understanding Private Mortgage Insurance (PMI)

Private Mortgage Insurance is often misunderstood but plays a crucial role in home financing. Here's what you need to know:

When PMI is required: Most lenders require PMI when your down payment is less than 20% of the home purchase price. This protects the lender if you default on the loan.

How PMI is calculated: PMI typically costs 0.5% to 1.5% of your loan amount annually, divided into monthly payments. The exact rate depends on your loan amount, down payment percentage, and credit score.

How to eliminate PMI: You can remove PMI by reaching 20% equity in your home through regular payments, or by refinancing when your home value increases significantly.

Try It Now: Our calculator automatically shows PMI costs when your down payment is less than 20%. Use the Advanced Options to adjust the PMI rate and toggle PMI on/off to see how it affects your monthly payment!

Key Numbers That Determine Your Loan

Several key factors influence the size and cost of your mortgage. Understanding them is key to finding the right loan for you.

Down Payment: This is the initial amount you pay upfront. A larger down payment reduces your loan amount, lowers your monthly payment, and can help you avoid Private Mortgage Insurance (PMI) if you put down 20% or more.

Try It Now: Curious how a larger down payment changes your monthly costs? Adjust the Down Payment slider on our calculator to instantly see the impact on your loan.

💡 PMI Insight: If your down payment is less than 20%, you'll typically need PMI. Our calculator automatically shows when PMI applies and exactly how much it adds to your monthly payment. You can adjust the PMI rate in Advanced Options to see different cost scenarios.

Loan Term: This is the length of your mortgage, typically 15 or 30 years. A shorter-term loan (like 15 years) has higher monthly payments but significantly less total interest paid over the life of the loan.

Try It Now: Use the Loan Term (Years) slider above to compare a 15-year vs. a 30-year loan. Notice how the monthly payment and total interest change dramatically.

Interest Rate: This is the percentage your lender charges for borrowing the money. It's influenced by the market, your credit score, and other factors.

Try It Now: Even a small change in interest rates can save you thousands. Move the Interest Rate (%) slider to see how your payment fluctuates.

The Power of Paying More: Amortization and Extra Payments

Amortization is the process of paying off your loan over time. In the beginning, more of your payment goes to interest. As you pay down the principal, more of your payment goes toward the loan balance. But you have the power to accelerate this process.

Making even small, regular extra payments toward your principal can have a massive impact, allowing you to:

Pay off your loan years earlier.

Save thousands, or even tens of thousands, of dollars in interest.

Try It Now: This is where you can save big. Use the Monthly Extra Payment ($) slider in our calculator to see how an extra $50 or $100 a month can shave years off your mortgage and save you a fortune in interest.

Property Tax Rates by State

Hover over any state to see its effective property tax rate. These rates are used in your mortgage calculations above.

Loading property tax map...

Effective Property Tax Rate

< 0.5%

0.5-0.7%

0.7-0.9%

0.9-1.1%

1.1-1.3%

1.3-1.5%

1.5-1.7%

1.7-1.9%

> 1.9%

Note: These are average effective property tax rates 2026. Your actual rate may vary based on local assessments and exemptions.

10 Essential Mortgage Tips

1. Master Your Mortgage Components

💡+

Our calculator focuses on Principal & Interest (PITI). Remember, your total housing payment (PITI) includes property taxes and homeowners insurance too!

2. Rate Shopping 101

🔍+

Don't settle for the first offer! Compare rates from multiple lenders to save thousands over the life of your loan.

3. Credit Score Magic

✨+

A higher credit score can get you lower interest rates. Check your report for errors and boost your score before applying.

4. Down Payment Power

💰+

A larger down payment reduces your loan amount, lowers your monthly PITI, and can help you avoid PMI if you put down 20% or more.

5. Loan Term Trade-offs

⚖️+

A 15-year mortgage has higher monthly payments but less total interest. A 30-year mortgage offers lower payments but more interest over time.

6. Closing Costs Alert

⚠️+

Don't forget closing costs! These fees can be 2-5% of your loan amount and include appraisals, title searches, and loan origination fees.

7. Pre-Approval Power

💪+

Pre-approval involves a lender reviewing your financial info and provides a conditional commitment for a specific loan amount.

8. PMI Decoded

🔍+

If your down payment is less than 20%, you'll likely pay PMI. This protects the lender and can be canceled once you reach 20% equity. Use our calculator to see exactly how much PMI adds to your monthly payment and explore strategies to eliminate it faster through extra payments.

9. Extra Payment Magic

✨+

Small additional payments towards your principal can shorten your loan term and save you a significant amount of interest. Try our debt repayment calculator to see how extra payments can accelerate your path to being mortgage-free.

10. Future Refi Options

🔄+

If interest rates drop or your financial situation improves, refinancing your mortgage could lower your payments or shorten your loan term. Check current mortgage rates and use our calculator to see if refinancing could save you money.

Interest Rate history

Explore our Interactive historical chart showing the 30 year fixed rate mortgage average in the United States from 1971-2026. Explore how interest rates have changed over time, impacting your mortgage payments.

Source: fred.stlouisfed.org

Mortgage Scenarios & Planning

How much house can I afford with an FHA loan?+

Calculate how much house you can afford with an FHA loan's lower down payment requirements (as low as 3.5%) and understand how FHA mortgage insurance impacts your monthly payments compared to conventional loans.

15-year vs 30-year mortgage payment comparison+

Compare monthly payments and total interest costs between 15-year and 30-year mortgage terms. The shorter term saves you thousands in interest despite higher monthly payments.

Monthly mortgage calculator with PMI and property tax+

Get a true picture of your monthly housing costs with our calculator that includes Principal, Interest, Taxes, Insurance (PITI), and Private Mortgage Insurance (PMI) when your down payment is less than 20%.

How extra payments affect mortgage principal+

Discover how making extra payments toward your principal can dramatically reduce your loan term and total interest paid. Even small additional amounts can lead to significant long-term savings.

Amortization schedule for 30-year fixed mortgage+

View a year-by-year breakdown of how each payment is split between principal and interest. See when you'll reach the "tipping point" where more of your payment goes toward principal than interest.

The 20% Down Payment Dilemma

Should you put down 20% to avoid PMI, or invest that money elsewhere? Use our calculator to compare scenarios and see the long-term impact on your finances.

The PMI Elimination Strategy

If you're paying PMI, discover how extra payments can help you reach 20% equity faster and eliminate this monthly cost. Our calculator shows exactly when PMI will be removed and how much you'll save.

The Refinance Decision

Interest rates dropped 1%? Calculate your break-even point for refinancing costs vs. monthly savings to make an informed decision.

The Extra Payment Strategy

See how adding just $100/month can save you $50,000+ in interest over your loan term and shave years off your mortgage.

Before applying for pre-approval

When comparing loan offers from different lenders

Before deciding on refinancing options

When planning extra payments to pay off early

When budgeting for your first home purchase

Frequently Asked Questions

Get instant answers about our interactive mortgage calculator and how real-time calculations can help you make smarter home buying decisions.

Our mortgage calculator provides real-time, live calculations that instantly update as you adjust any slider or input field. Unlike static calculators that require you to click "calculate" after each change, our dynamic tool shows immediate results for monthly payments, total interest, and payoff scenarios.

This interactive approach lets you explore different scenarios effortlessly - adjust your down payment, loan term, or interest rate and watch how each change impacts your mortgage payments in real-time.

Our mortgage calculator uses industry-standard formulas and provides highly accurate estimates for your monthly payments, including principal, interest, taxes, and insurance (PITI). The live calculations update instantly using the same mathematical principles that lenders use.

However, remember that these are estimates. Your actual mortgage terms may vary based on your credit score, debt-to-income ratio, and specific lender requirements. Always consult with a qualified mortgage professional for final loan details.

Yes! Our interactive calculator includes a live extra payment slider that instantly shows how additional monthly payments can reduce your total interest and shorten your loan term. Simply adjust the extra payment amount and watch the payoff time decrease in real-time.

This feature helps you visualize the powerful impact of even small extra payments - you might be surprised how much you can save over the life of your loan!

Our advanced options include real-time calculations for:

Property Tax: Adjust the annual property tax rate to see its impact on your monthly payment

Homeowners Insurance: Include insurance costs in your total monthly housing payment

HOA Fees: Factor in homeowners association fees for a complete picture

All these inputs update your total monthly payment instantly, giving you a comprehensive view of your true housing costs.

Simply use the loan term slider to switch between 15-year, 30-year, or any custom loan term. The calculator instantly shows how different terms affect your:

Monthly Payment: Shorter terms = higher monthly payments but less total interest

Total Interest: Longer terms = lower monthly payments but more total interest paid

This real-time comparison helps you find the perfect balance between affordable monthly payments and total loan cost.

Absolutely! Our calculator offers both percentage and dollar amount inputs for down payments. As you adjust either slider, you'll instantly see how your down payment affects:

• Your loan amount and monthly payments

• Whether you'll need PMI (Private Mortgage Insurance)

• Your total interest over the life of the loan

This helps you determine the optimal down payment strategy for your financial situation.

Very sensitive! Our live interest rate slider demonstrates this clearly. Even a 0.25% rate change can significantly impact your monthly payment and total interest paid over the loan term.

Use our real-time calculator to see exactly how rate changes affect your specific loan amount. This insight is crucial when timing your mortgage application or deciding whether to pay points to buy down your rate.

Yes! Our interactive calculator is perfect for refinancing analysis. Input your current loan balance as the home price, set your down payment to $0, and adjust the interest rate to see potential savings with a new loan rate.

The real-time calculations instantly show you how a lower rate could reduce your monthly payments or how switching loan terms might affect your total interest paid. This helps you quickly determine if refinancing makes financial sense.

AI provides static mortgage calculations, but our interactive tool lets you explore scenarios with rate sliders, see visual amortization charts update in real-time, and compare different loan terms side-by-side - all unavailable through AI text responses. When you want to explore "what-if" scenarios, see how rate changes affect total interest, visualize different down payment impacts, or need hands-on mortgage scenario modeling that AI cannot provide, our tool is the better choice.

A general guideline is the 28/36 rule. This suggests that your monthly housing costs shouldn't exceed 28% of your gross monthly income, and your total debt (including housing) shouldn't exceed 36%. Our calculator helps you test different scenarios to see what's comfortable for your budget.

The 28/36 rule is a guide for lenders to assess your borrowing capacity. It states that your housing expenses (principal, interest, taxes, and insurance) should not be more than 28% of your gross monthly income, and your total debt-to-income ratio (DTI) should not exceed 36%.

Our calculator makes it easy! Simply expand the "Advanced Options" section and enter your estimated monthly property taxes and homeowner's insurance. The calculator will automatically add these to your principal and interest payment to show you a more accurate total monthly housing cost (PITI).

While a 20% down payment is often recommended to avoid private mortgage insurance (PMI), many conventional loans are available with as little as 3% down. FHA loans require as little as 3.5% down. Use our calculator to see how different down payment amounts affect your monthly payment and total interest paid.

PMI Consideration: If your down payment is less than 20%, you'll typically need PMI, which adds $42-$125 monthly for every $100,000 borrowed. However, you can remove PMI once you reach 20% equity through payments or home appreciation. Our calculator automatically shows PMI costs and when they'll be eliminated.

Private Mortgage Insurance (PMI) is an insurance policy that protects lenders in case you default on your mortgage. It's typically required when your down payment is less than 20% of the home price. PMI allows you to buy a home with a smaller down payment, but it adds to your monthly mortgage payment.

The cost of PMI varies based on your loan amount, down payment percentage, and credit score. Our calculator shows you exactly how much PMI adds to your monthly payment when your down payment is less than 20%.

You can remove PMI in several ways:

• Reach 20% equity: Once you've paid down your mortgage to 80% of the original loan amount, you can request PMI cancellation

• Automatic termination: PMI automatically terminates when you reach 78% of the original loan amount through normal payments

• Refinancing: If your home has appreciated significantly, you may be able to refinance into a loan without PMI

• Extra payments: Making extra payments toward your principal can help you reach the 20% equity threshold faster

PMI typically costs between 0.5% to 1.5% of your loan amount per year, which works out to $42 to $125 per month for every $100,000 borrowed. The exact cost depends on:

• Your loan amount

• Your down payment percentage

• Your credit score

• The type of loan (conventional vs. FHA)

Use our calculator's Advanced Options to adjust the PMI rate and see exactly how it affects your monthly payment. You can also toggle PMI on/off to compare payments with and without it.

🏠 Perfect Complement to AI Advice: Use AI to understand mortgage concepts and get general financing guidance, then use our interactive tool to explore those concepts with your specific numbers. Slide through interest rates, compare different loan terms, and visualize how extra payments affect your amortization schedule - creating a complete home financing experience that combines AI's expertise with hands-on scenario testing.